Volatility is Back, One Year Later

In a Nutshell

- Escalating conflict in the Middle East—triggering a surge in oil prices—combined with U.S. policy developments and more hawkish central bank signals, led to heightened volatility, rising yields, and a broad repricing of risk across global markets.

- Equities posted significant losses across the U.S., Europe, and emerging markets, while bond yields rose sharply due to renewed inflation fears linked to energy shocks; credit spreads widened, and commodities (notably oil) outperformed, while gold declined.

- Discretionary portfolios lagged benchmarks primarily due to equity allocation (notably U.S. SMID caps and tech concentration) and negative contributions from alternatives, while lower duration and an underweight in fixed income partially mitigated losses.

March 2026 will be remembered as a month when geopolitical shockwaves from the Middle East collided with policy shifts in Washington and cautious recalibrations by central banks, sending ripples through US and European financial markets.

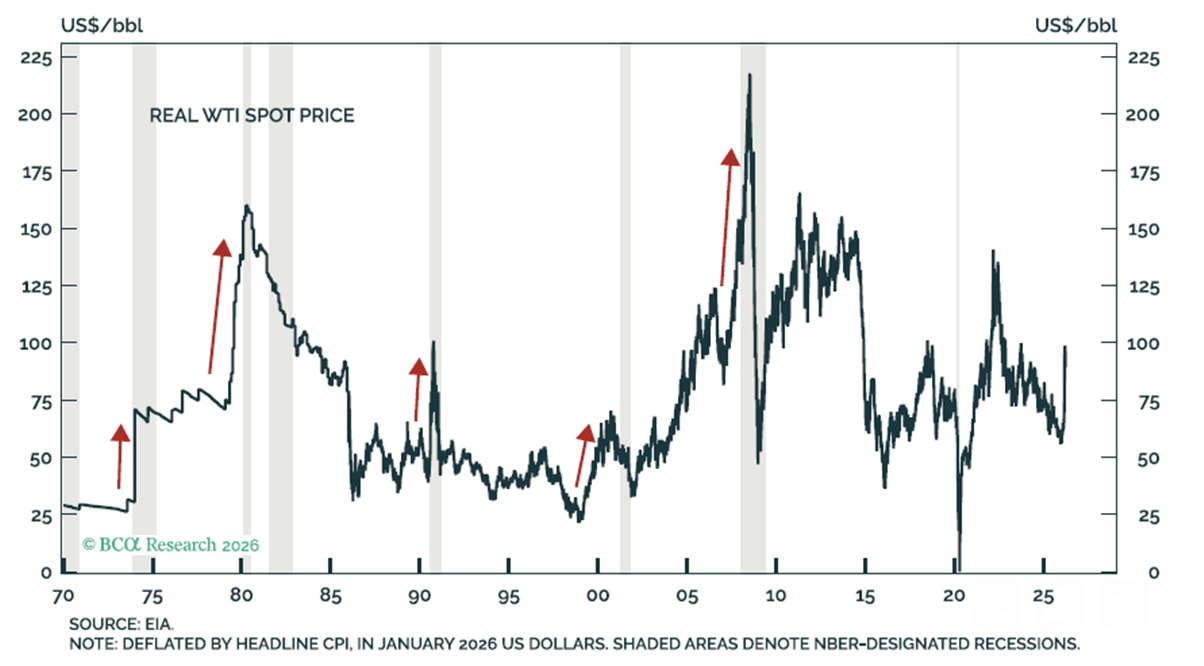

The drama unfolded dramatically in the final days of February, with the effects dominating March trading. Coordinated US and Israeli military strikes on Iran killed Supreme Leader Ayatollah Ali Khamenei and several top officials, triggering retaliatory attacks and fears of broader disruption to global energy supplies. Oil prices exploded higher, with Brent crude surging more than 50% for the month at points and US West Texas Intermediate briefly topping $100 per barrel. Energy and defense stocks rallied sharply on both sides of the Atlantic, while broader equities—particularly growth-oriented names—faced selling pressure amid stagflation concerns. European markets, more exposed to energy imports, showed heightened sensitivity, with the Stoxx 600 and national benchmarks like the DAX and FTSE experiencing volatile swings and periods of underperformance.

Just as investors grappled with this new “war premium,” a landmark US Supreme Court ruling offered a brief counterbalance. In a decision handed down in February but with ongoing market implications into March, the Court invalidated large portions of President Trump’s sweeping tariffs imposed under the International Emergency Economic Powers Act (IEEPA). The ruling curbed executive authority to levy broad “reciprocal” and emergency tariffs, easing some trade-war fears and providing a modest lift to US importers, consumer stocks, and European exporters sensitive to transatlantic flows. Market participants considered it one of the most significant non-military developments of the period, though uncertainty persisted over alternative tariff tools the administration might pursue.

Mid-month brought a high-stakes “Super Thursday” of central bank decisions. The Federal Reserve, European Central Bank, Bank of England and others largely held rates steady, but their accompanying statements reflected a more hawkish tilt. Officials highlighted potential upside inflation risks from elevated energy costs and the conflict’s broader economic shock, while growth forecasts were tempered. ECB President Christine Lagarde described the Middle East situation as “a real shock,” and markets rapidly repriced for fewer rate cuts—or even potential tightening—later in the year. This shift weighed on rate-sensitive sectors, contributed to higher long-term yields, and added to pressure on technology and growth stocks already bruised by geopolitical uncertainty.

Throughout the month, mixed economic data releases amplified the sense of fragility. US inflation readings remained sticky, while employment reports painted a picture of a softening labor market: February payrolls showed outright job losses in several key sectors, unemployment claims edged higher, and wage growth slowed, all signaling that the energy shock was beginning to weigh on hiring and consumer confidence. Eurozone figures told a similar story of moderating momentum. Oil price volatility—fueled by repeated threats to the Strait of Hormuz and infrastructure risks—kept energy sectors in focus while acting as a headwind for consumer and cyclical names. Safe-haven assets, including gold and certain government bonds, saw episodic demand.

In the end, March 2026 illustrated how quickly external shocks can reshape market narratives. The combination of geopolitical tensions, judicial intervention on trade policy, and central banks navigating an uncertain inflation-growth trade-off left investors in a risk-off posture, rotating toward defensives and commodities while closely monitoring developments in the Gulf region. As the quarter closed, markets remained on edge, with the trajectory of Middle East tensions continuing to overshadow traditional economic drivers.

Financial Market Returns

During the month, U.S. equity indices posted significant losses, with the S&P 500 down -4.98% and the tech-heavy Nasdaq 100 declining -4.81%, followed by the MSCI World index (-6.32%). Losses were even more pronounced in Europe and emerging markets, which are more exposed to energy flows from the Gulf region. The STOXX Europe 600 fell -7.54%, while emerging markets declined -13.04%, also weighed down by the strengthening U.S. dollar and the collapse of the South Korean equity market (-19%).

In fixed income, uncertainty surrounding the duration of the conflict and potential disruptions to global energy supply fueled concerns of renewed inflationary pressures. Government bond yield curves shifted sharply higher across maturities. At its meeting on 17-18 March, the Federal Reserve left interest rates unchanged; furthermore, Chairman Powell’s comments were seen as a cautions, wait-and-see approach to assessing the impact of tariffs and the energy situation.

In this environment, 2-year yields rose by more than 50 basis points in both the U.S. and Europe, reaching 3.79% in the U.S. and 2.61% in Germany, while Swiss 2-year yields returned to positive territory at 0.07% (from -0.16% the previous month). Ten-year yields also moved significantly higher, with U.S. Treasuries closing at 4.32% after briefly approaching the 4.50% threshold, while German Bunds reached 3.00% and Swiss government bonds 0.34%.

In credit markets, corporate bonds experienced broad-based widening in spreads. In the U.S., investment grade returned -1.98% and high yield -1.13%. In Europe, the decline was slightly more pronounced, with investment grade declining -2.26% and high yield -2.69%. Emerging market bonds also ended the month in negative territory (-2.23%).

The commodities complex was the standout performer, with oil rising by more than 50% month-on-month and Brent approaching USD 120 per barrel. Markets experienced heightened volatility, driven by news of attacks on tankers and energy infrastructure. The Iranian regime’s tenacity has come as a surprise, as a short-lived conflict had initially been expected. With the Strait of Hormuz still closed after more than a month, and uncertainty remaining elevated, markets continue to weigh potential risks of escalation alongside signs of de-escalation in the region.

In this context, gold declined by -11.57%, closing at USD 4,668.06 per ounce. The counter-intuitive performance reflects profit-taking following the strong rally in recent years, as well as the impact of expectations for potentially tighter monetary policy.

In currency markets, the U.S. dollar strengthened significantly, closing at 1.1553 against the euro and 0.7995 against the Swiss franc. Key drivers included rising bond yields, with reduced expectations for rate cuts.

Lastly, Bitcoin recovered from earlier weakness ending the month in positive territory at USD 68,193.95.

Portfolio Commentary

In March, our discretionary portfolios underperformed their benchmark.

Within fixed income, our relative lower duration compared to the benchmark helped mitigate the negative impact on the portfolio of the increase in inflation expectations that followed the beginning of the conflict in Iran, with positive contribution distributed across all the sleeves in the asset class. Furthermore, the downside pressure affected all maturities in the term structure of the interest rates of the U.S. yield curve, translating in a parallel shift that left no safe spots expect for cash. On top of that, our relative underweight in fixed income provided a positive allocation effect, helping reduce the losses from the asset class correction.

Equities were the main drag on relative performance. The strategic allocation in U.S. Small and Mid-Caps resulted in a source of detraction as increasing interest rates led investors to review their positions in size equities due to headwinds consisting in higher cost of financing and rising recession probabilities. Moreover, the uncertainty over the potential length of the war drove down the valuations of broader indexes too, with investors fearing a potential 2022-like scenario, resulting in negative returns in beta related positions as well. Finally, despite the stabilization of the U.S. software sector, concentration in Microsoft kept adding detraction as the combined effect of market-wide pressure on big tech and less-than-expected Q4 2025 results didn’t manage to offset the positive sentiment on the company. Diversification in international equities didn’t prove beneficial either, but the relative underweight in Emerging Markets compared to the benchmark helped reduce exposure to the larger drawdowns recorded in the region.

The detraction in alternative investments didn’t stop in March, with private-equity allocations delivering negative selection effects due to the concerns of AI disruptions on the private software sector, while in commodities the allocation toward gold was, for once, a negative detractor, due to the increase in real yields amid elevated geopolitical uncertainty.

Over the period, we have closed our position in U.S. Small and Mid-Caps in order to increase the exposure to Emerging Markets, aligning it with the benchmark.

Sources: Capital Economics, Bloomberg, BCA, Empirical Research, Hussmann, WSJ, Ned Davis, mrbPartners, LFA.

This material is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Past performance does not guarantee future results, and all investments involve risk, including potential loss of capital. Any forward-looking statements are inherently uncertain and subject to change. References to specific securities are for attribution only and should not be construed as a recommendation. Third-party data are believed to be reliable but are not guaranteed and may change without notice.