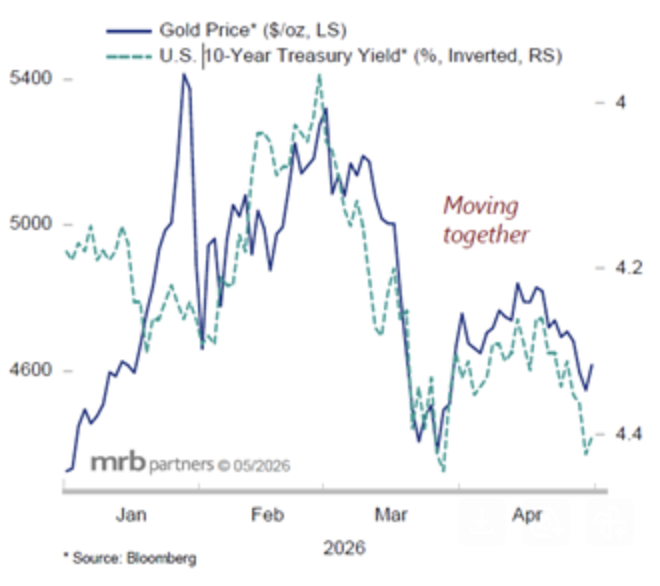

Recent Weakness Reflects Macro Pressures More Than Geopolitical Dynamics

Despite its longstanding reputation as a potential safe-haven asset against geopolitical risk and inflation, gold has declined by roughly the mid-teens in percentage terms since the start of the conflict in the Middle East. The recent move highlights how, in the current environment, bullion is trading less as a pure safe-haven asset and more as a macro-sensitive instrument, with short-term performance largely dictated by real yields, the dollar and investor positioning.

The most immediate drag has been the pronounced rise in nominal and real government bond yields. As investors have repriced the outlook for tighter monetary conditions and more persistent inflation, the opportunity cost of holding a non-yielding asset such as gold has increased significantly. At the same time, the strength of the US dollar, supported by firmer relative real rates, has added further pressure.

Demand dynamics have also become less supportive. Official-sector buying has moderated after a period of exceptionally strong accumulation, while some reserve holders have turned more cautious as liquidity needs have risen. Meanwhile, private demand has become increasingly tactical and leveraged, making gold more vulnerable to episodes of deleveraging in which investors sell bullion to raise cash, thereby amplifying downside moves.

What Will Drive Gold From Here

The recent correction confirms that gold prices are currently being driven primarily by rates, currency moves and speculative flows rather than by geopolitical headlines alone. Over the coming months, any further upside in nominal and real yields, continued dollar resilience and additional unwinding of leveraged positioning could keep bullion under pressure.

That said, the medium-term underpinnings of the asset class remain constructive. Persistently loose fiscal policy and rising public debt continue to sustain concerns over the long-term debasement of fiat currencies, while inflation is still expected to settle structurally above the unusually subdued levels that characterized the pre-2019 period. In parallel, growing uncertainty around the long-term role of the dollar within the global financial system and a structurally higher geopolitical risk premium continue to support the strategic appeal of non-defaultable reserve assets.

In other words, recent price weakness does not invalidate the longer-term constructive case for gold; rather, it illustrates that short-run trading remains dominated by macro variables that can temporarily overwhelm structural demand. As the upward pressure on real yields and the dollar begins to moderate, the backdrop for bullion should gradually become more favorable again.

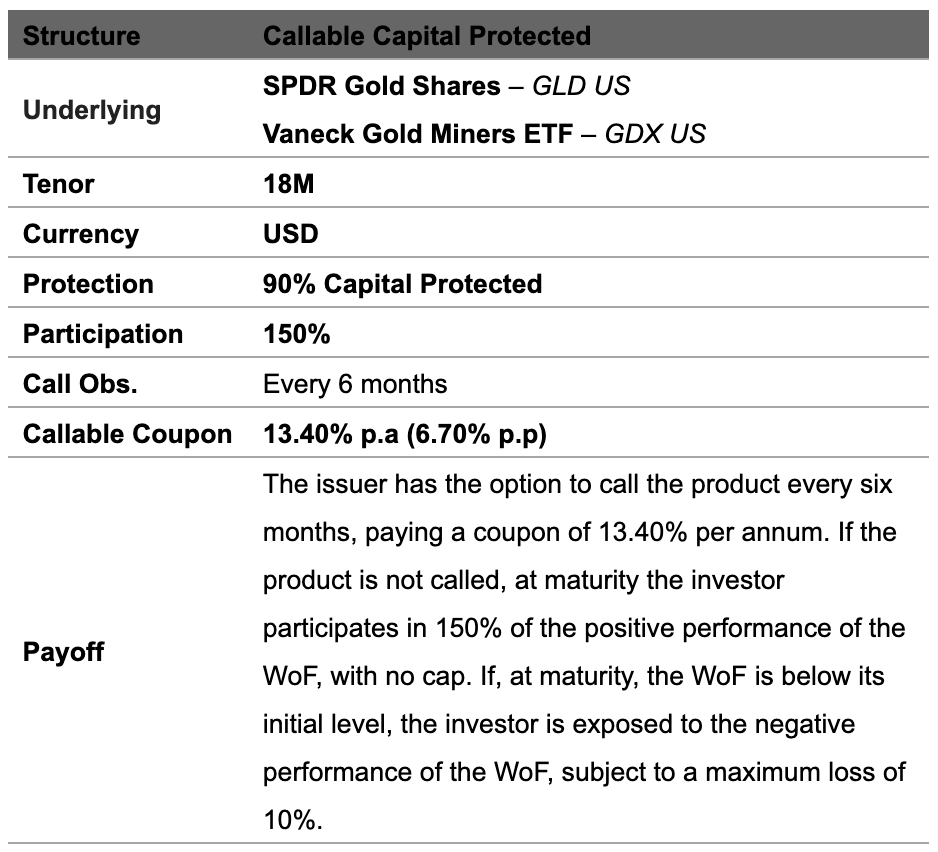

Investment Idea

The current market backdrop – characterized by elevated uncertainty and sharp volatility across gold and gold mining equities year-to-date, per Bloomberg data – may present a potentially notable opportunity for certain investors seeking exposure to this space with partial capital protection. The structured note we are presenting provides two potential sources of return: on the one hand, an indicative coupon of 13.4% per annum, should the issuer exercise its early call option; on the other, leveraged participation (150%) in the upside performance of the worst-of basket composed of gold and gold miners, should the product remain outstanding until maturity. The product provides partial capital protection; however, investors remain exposed to downside risk, with a maximum loss of 10% of invested capital at maturity.

Key Risks: This product carries material risks that investors should carefully consider before investing: (i) the coupon is only paid if the issuer exercises the call option, which is not guaranteed; (ii) if the product is not called, the investor’s return depends entirely on the performance of the worst-performing asset in the basket (GLD or GDX), which could result in a loss of up to 10% of capital; (iii) gold and gold mining equities are subject to significant price volatility driven by interest rates, currency movements, commodity prices, and broader market conditions; (iv) the 90% capital protection applies only at maturity and not if the product is sold in the secondary market before maturity; (v) investors are exposed to the credit risk of the issuer. This communication is for informational purposes only and does not constitute a solicitation or offer to invest.

90% Capital Protection With Participation on the Worst-of (WoF)

This material is a marketing communication and is for informational purposes only. It does not constitute investment research, advice, a recommendation, or an offer to buy or sell any security or financial instrument. Past performance, including historical returns, prices, or yields, is not indicative of future results, and all investments involve risk, including loss of capital. Opinions, estimates, and forward-looking statements contained herein reflect LFA’s views at the time of writing and are not guarantees or forecasts. References to specific securities, indices, commodities, currencies, or cryptocurrencies are for illustrative purposes only and should not be construed as recommendations. Numerical examples and scenario analyses are based on assumptions that may change. Third-party data are believed to be reliable but are not guaranteed and may be revised. Readers should consult qualified financial, tax, and legal advisors regarding any investment, financial, or tax decision. Nothing in this material constitutes legal, tax, or accounting advice.