- Tensions in the Middle East remain unresolved

- The earnings season confirmed resilience

- Macroeconomic data pointed to a late-cycle dynamic

From Shock to Complex Stabilization

April 2026 marked a transition from the geopolitical shock of March toward a more stable—though still uncertain—macro environment. While tensions in the Middle East remained unresolved, the lack of further escalation reduced immediate risks to global energy supply. Oil prices, after a brief retracement, moved higher again, continuing to pose upside risks to inflation (as of writing, they are coming down again). So far, the increase has been largely confined to energy components, but a prolonged shock could broaden inflationary pressures, with implications for interest rates.

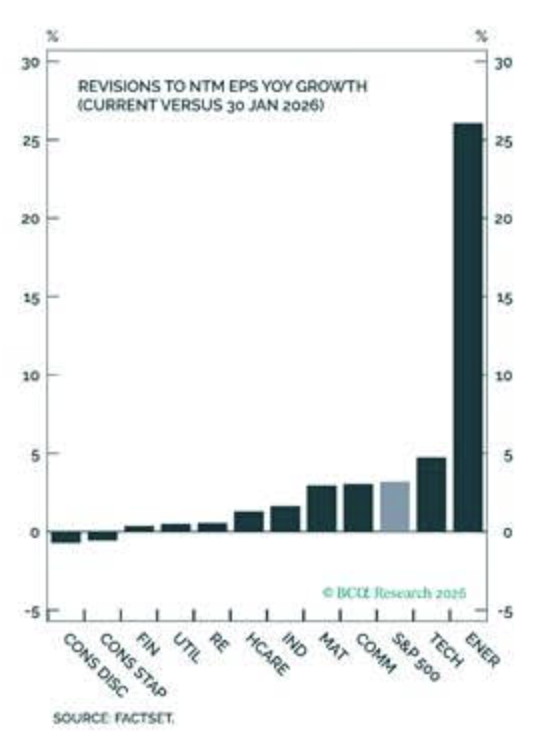

In the United States, the earnings season confirmed resilience in key sectors, particularly energy and large-cap technology, the latter supported by ongoing investment in artificial intelligence.

At the same time, macroeconomic data pointed to a late-cycle dynamic: inflation remained sticky, while recent labor market indicators suggested renewed tightness. Given the recency of these data, revisions remain possible, but the trend requires close monitoring. A simultaneous rise in both input costs and wages would limit central banks’ flexibility and could trigger a renewed tightening cycle, with negative implications for asset prices. Partially offsetting these risks, productivity has remained strong in recent quarters. Consumer sentiment, however, continued to reflect the impact of higher energy costs.

In Europe, economic data remained weak, with manufacturing still in contraction and services showing signs of slowing momentum. Policymakers maintained a cautious stance, with both the Federal Reserve and the European Central Bank emphasizing data dependency and uncertainty around the inflation outlook.

April also saw increased policy activity. In the United States, regulatory pressure intensified in the healthcare sector, particularly on pharmacy benefit managers, signalling growing political scrutiny. In Europe, targeted interventions in energy pricing confirmed governments’ willingness to act on consumer costs. In China, authorities introduced selective stimulus measures to support credit and infrastructure. While these measures provided some support, they also risk exacerbating overcapacity and increasing reliance on exports, potentially heightening trade tensions with both the United States and Europe.

Against this complex backdrop, market attention has increasingly turned to capital markets activity. Following a pickup in deal-making in 2025, expectations for 2026 point to a strong M&A and IPO pipeline, with high-profile potential listings including SpaceX, Anthropic, OpenAI, Databricks, and Canva. These transactions could absorb significant market liquidity, which remains ample for now. More broadly, M&A activity deserves scrutiny: when strategic rationale becomes less clear, it may signal late-cycle behavior. In this context, reported discussions around a potential bid by GameStop for eBay stand out as an example of increasingly aggressive deal dynamics.

Overall, April reflected a shift from acute crisis to a more complex environment shaped by persistent inflation, slowing growth, and ongoing geopolitical and policy uncertainty. Markets are now driven less by immediate shocks and more by the interaction between policy decisions, macro data, and structural risks.

Markets

Equities U.S. equity indices posted particularly strong gains, with the S&P 500 rising +10.49% and the Nasdaq 100 +15.66%. The MSCI World followed with a +9.64% increase, while the STOXX Europe 600, more exposed to Middle Eastern energy dynamics, recorded a more moderate gain of +5.56% in local currency terms. Emerging markets also delivered a strong performance, closing the month up +14.74%. At the sector level, technology and semiconductors led the rally, while the defense sector underperformed amid expectations of a potential peace agreement.

Fixed Income Government bond yields moved higher, reflecting ongoing inflation concerns. Yield curves steepened across both short and long maturities. The U.S. 2-year Treasury yield closed at 3.87%, while its German and Swiss counterparts reached 2.64% and 0.13%, respectively. Ten-year yields followed a similar trend, with the U.S. Treasury at 4.37%, approaching the key 4.50% threshold, while German Bunds and Swiss government bonds closed at 3.04% and 0.38%, respectively.

In credit markets, following the spread widening observed in March, April saw a reversal in trend, with positive returns across all major segments. In the U.S., investment-grade bonds gained +0.45% and high yield +1.63%. In Europe, investment grade rose +0.94% and high yield +1.80%. Emerging market bonds also delivered a robust performance, closing the month up +2.53%.

Commodities After the sharp rally in March, oil prices traded with elevated volatility, fluctuating between USD 100 and 120 per barrel depending on geopolitical developments. Gold declined slightly to USD 4,617.85 per ounce (-1.08%), followed by silver (-1.89%).

Currencies In currency markets, the U.S. dollar initially strengthened against major currencies before weakening toward month-end, driven by the Middle East truce and less concerning inflation data. The EUR/USD exchange rate closed at 1.1731, while USD/CHF ended at 0.7814. Lastly, Bitcoin recorded a strong month, gaining +12.13% and closing at USD 76,466.34.

Performance Commentary

In April, discretionary portfolios delivered positive performance across asset classes, consistent with a relatively prudent positioning, while markets favored higher-beta and more volatile segments.

The fixed income allocation generated moderate positive returns, slightly outperforming global bond markets over the month.

Equities rebounded strongly across regions and sectors. However, some long-term core positions—such as Microsoft and Cybersecurity—lagged the sharp rally in the semiconductor segment, which dominated market leadership.

The semiconductor-driven momentum particularly supported markets like Taiwan and South Korea, which remain relatively underrepresented in our emerging markets allocation. Nevertheless, our emerging markets exposure, which is more fundamentally driven, also posted strong gains.

In alternatives and commodities, performance was broadly in line with the market overall. Within commodities, our overweight to gold and limited exposure to diversified commodity indices acted as a drag on relative returns during April.

Transactions

During the period, the Investment Committee decided to increase the duration of the portfolio, now closer but still lower than the benchmark, confirming our cautious stance against duration risk.

Sources: Capital Economics, Bloomberg, BCA, Empirical Research, Hussmann, WSJ, Ned Davis, MRB Partners, LFA.

This material is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Past performance does not guarantee future results, and all investments involve risk, including potential loss of capital. Any forward-looking statements are inherently uncertain and subject to change. References to specific securities are for attribution only and should not be construed as a recommendation. Third-party data are believed to be reliable but are not guaranteed and may change without notice.