So…How Did It Go?

As the year drew to a close, December ushered in a fresh wave of uncertainty for both the global economy and the geopolitical landscape. In the United States, incoming data increasingly pointed to a K-shaped economy—one that, by its very nature, complicates any clear assessment of where growth is heading. On the one hand, the labor market continued its gradual deterioration: initial jobless claims have risen steadily without being offset by sufficient new hiring, pushing the unemployment rate up to 4.6%. Manufacturing remains firmly in contraction territory—an almost normalized condition that now barely registers in headlines—while consumer confidence among average households is deeply depressed. On the other hand, retail sales proved resilient, buoyed in part by the onset of the holiday season. Once again, this underscored the growing divergence within the U.S. consumer base, where a relatively small segment of higher-income households accounts for a disproportionate share of overall demand. Consistent with the central role of consumption in U.S. output, third-quarter GDP revisions came in exceptionally strong, at 4.3% annualized. Inflation also surprised to the downside, with core CPI easing to 2.6% year-over-year for the September–November period—well below consensus expectations. That said, this reading should be interpreted cautiously, as it may have been distorted by temporary factors, including the recent government shutdown. Greater clarity is likely to emerge with January’s release, which market expectations currently place around 2.7% year-over-year.

As the year drew to a close, December ushered in a fresh wave of uncertainty for both the global economy and the geopolitical landscape. In the United States, incoming data increasingly pointed to a K-shaped economy—one that, by its very nature, complicates any clear assessment of where growth is heading. On the one hand, the labor market continued its gradual deterioration: initial jobless claims have risen steadily without being offset by sufficient new hiring, pushing the unemployment rate up to 4.6%. Manufacturing remains firmly in contraction territory—an almost normalized condition that now barely registers in headlines—while consumer confidence among average households is deeply depressed. On the other hand, retail sales proved resilient, buoyed in part by the onset of the holiday season. Once again, this underscored the growing divergence within the U.S. consumer base, where a relatively small segment of higher-income households accounts for a disproportionate share of overall demand. Consistent with the central role of consumption in U.S. output, third-quarter GDP revisions came in exceptionally strong, at 4.3% annualized. Inflation also surprised to the downside, with core CPI easing to 2.6% year-over-year for the September–November period—well below consensus expectations. That said, this reading should be interpreted cautiously, as it may have been distorted by temporary factors, including the recent government shutdown. Greater clarity is likely to emerge with January’s release, which market expectations currently place around 2.7% year-over-year.

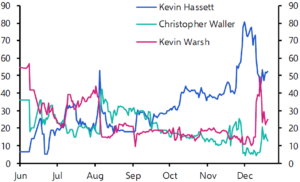

Against this backdrop, the Federal Open Market Committee (FOMC) adopted a dovish policy stance while maintaining hawkish rhetoric. For the third consecutive meeting, the Fed cut its policy rate by 25 basis points, bringing the target range to 3.50%–3.75%. Yet its projections for 2026 depict an economy growing at a solid 2.3%, inflation remaining above target, and unemployment declining from current levels. Chair Powell expressed confidence that the inflationary effects of tariffs would prove transitory, suggesting the Committee may pause further easing over the coming months. Financial markets appear broadly aligned with this wait-and-see approach, pricing in two rate cuts in 2026 versus just one implied by the Fed’s own projections. The true wildcard, however, lies in the impending leadership change at the Fed in May, when Powell is set to be replaced by President Trump’s nominee. While the successor has yet to be named, it is widely assumed that the new chair may favor a more aggressive push toward lower interest rates than currently envisaged.

As I reflect on the major events of this final month of the year, it is hard not to wonder whether the world has fundamentally changed over the past decade—whether it has truly become more dangerous—or whether our perception has instead been reshaped by an unrelenting news cycle and the amplifying force of social media. Perhaps it is both. What is beyond doubt is that December confirmed 2025 will be remembered as an eventful and turbulent year. In this single month alone, we witnessed U.S. strikes and embargoes targeting Venezuelan facilities and drug-trafficking vessels in the Caribbean and Pacific; widespread protests in Iran triggered by economic collapse and sanctions; a mass shooting at Sydney’s Bondi Beach that claimed 15 lives; a tragic New Year’s Eve in Crans-Montana resulting in more than 40 fatalities; and the emergence of a large-scale, still-unfolding fraud scandal in Missouri (with apologies for any significant events inadvertently omitted).

There were, of course, brighter developments worth acknowledging. For example, scientists confirmed that the Antarctic ozone hole reached its smallest size in six years—tangible evidence of the Montreal Protocol’s long-term success in safeguarding Earth’s atmosphere. Yet, more broadly, 2025 was a difficult year marked by conflict and disruption, and such positive milestones often struggled to break through the noise.

I would nonetheless like to end on a lighter note—with a curiosity borrowed from a newsletter I follow. In navigating the unpredictable, the author observed, unpredictability itself can at times become…predictable. When it comes to the U.S. administration, one such unconventional signal is the so-called Pentagon Pizza Index. The premise is simple: according to popular media anecdotes, unusual spikes in late-night pizza orders near the Pentagon have historically preceded major military operations or pivotal geopolitical decisions. For instance, the index surged at 2:04 a.m. ET on January 3rd and remained elevated until shortly after 3:00 a.m.; by 3:44 a.m., activity had dropped sharply. The timing coincided with explosions reported in Caracas and a subsequent public announcement by President Donald Trump. Similar patterns were observed ahead of recent Middle East offensives, including Israeli actions against Iran. So, perhaps there is no need for elaborate hedging strategies after all—sometimes, a stroll through the Pentagon’s neighborhood may suffice.

December serves as a fitting epilogue to a year defined by a disorderly transition from post-pandemic normalization to a far more fragmented and policy-driven economic regime—one in which geopolitics and economics repeatedly collided. The year began with the Federal Reserve entrenched in a “higher for longer” posture as inflation remained stubborn and consumer resilience endured. Over time, however, momentum became increasingly uneven as the new administration’s aggressive trade policies, tighter immigration stance, and cuts to the federal workforce contributed to heightened uncertainty in prices, confidence, and investment. By spring, the escalation surrounding “Liberation Day” tariffs—and the subsequent stop-start reversals—accelerated the sense that globalization was giving way to a more protectionist order, widening the gap between buoyant financial markets and large corporates on the one hand, and a more strained Main Street on the other, particularly among lower-income households.

Growth slowed but never fully broke. Trade distortions—from import front-running to abrupt reversals—periodically inflated headline GDP even as underlying domestic demand softened. The labor market showed increasing signs of strain through weaker prints and sizable downward revisions, while long-dated yields rose in response to mounting fiscal concerns and a swelling deficit. Central banks followed divergent yet converging paths: the ECB cut rates amid fragile growth and political stress, China relied on targeted support, and the Fed eventually began easing despite inflation remaining above target. Meanwhile, U.S. corporate earnings remained impressively strong—driven largely by AI-exposed mega-caps—even as forward guidance grew more cautious and valuations left little margin for error. Late-year developments added further complexity: a sharp but short-lived Middle East shock, a prolonged U.S. government shutdown that complicated economic readings and contributed to volatility, and partial trade de-escalation with key partners. Together, these forces reinforced the defining theme of 2025—an economy that continued to muddle through, but with structural risks from trade fragmentation, fiscal imbalance, and an increasingly bifurcated consumer becoming ever harder to ignore.

During the final month of the year, equity markets delivered mixed performances. The Stoxx Europe 600 closed December with a solid gain of +2.82%, followed by the MSCI World (+0.84%), while U.S. indices recorded more subdued results. The S&P 500 ended the month broadly flat (+0.06%), whereas the Nasdaq 100 declined slightly (–0.67%). Mid-month, U.S. equities came under pressure amid renewed concerns surrounding artificial intelligence, triggered by Broadcom’s earnings release, which fell short of investor expectations, and Oracle’s announcement of delays in several data center–related projects. Sentiment improved later in the month, however, following the release of U.S. inflation data below expectations and a strong third-quarter 2025 GDP growth print of +4.3%, well above consensus estimates.

On a full-year basis, equity market performances were robust and uniformly in double-digit territory, supported by continued enthusiasm for artificial intelligence and the resumption of the Federal Reserve’s rate-cutting cycle. This occurred despite periods of heightened volatility earlier in the year, driven by factors such as the DeepSeek episode and tariff-related developments, such as Liberation Day. The MSCI World emerged as the top-performing index in 2025 (+21.63%), followed by the Nasdaq 100 (+21.02%), the Stoxx Europe 600 (+20.65%), and the S&P 500 (+17.86%), all in local currencies.

In fixed income markets, investor attention remained firmly focused on central bank decisions, particularly forward guidance regarding the future path of monetary policy. As noted previously, the Federal Reserve cut interest rates by 25 basis points at its December meeting, while the European Central Bank left rates unchanged, in line with expectations. Against this backdrop, credit markets exhibited divergent dynamics. Investment-grade bonds declined by 29 basis points in USD terms and by 0.19% in Europe, while the high-yield segment posted positive returns of +0.69% in USD and +0.37% in EUR. Emerging market bonds also delivered positive performance (+0.30%, in USD terms). In government bond markets, yields at the long end of the curve moved higher across the U.S., Germany, and Switzerland, with 10-year yields closing at 4.17%, 2.85%, and 0.28%, respectively. At the short end, the U.S. 2-year yield edged slightly lower to 3.47%, while it rose in Germany (2.12%) and Switzerland (–0.09%).

Overall, 2025 proved to be a positive year for fixed income as an asset class. Investment-grade and high-yield indices in USD gained +7.78% and +8.50%, respectively, while their European counterparts rose by +3.03% and +5.15%. Emerging market bonds also recorded a strong annual performance (+8.73%, in USD terms).

Within commodities, oil prices declined for the fifth consecutive month. Both WTI and Brent moved lower following Iraq’s decision to bring back online a facility accounting for approximately 0.5% of global production. Sanctions imposed by the Trump administration on tankers entering and exiting Venezuela, as well as the potential for additional sanctions on Russian oil exports in the absence of a peace agreement with Ukraine, provided some support to prices, though not enough to reverse the monthly decline. On a full-year basis, oil prices fell by approximately 20%, marking the third consecutive year of negative performance. Gold, by contrast, extended its positive trend even in the final month of the year, rising +1.89% to close at USD 4,319.37 per ounce and delivering an exceptional annual performance of +64.58%. The rally was supported by the rate-cutting cycle, persistent geopolitical risks, and substantial central-bank purchases. Silver benefited from the same environment, more than doubling over the year, rising from USD 28.90 to USD 71.66 per ounce (+147.95%).

In currency markets, the U.S. dollar weakened following the Federal Reserve’s December rate cut, closing at 1.1746 against the euro and 0.7926 against the Swiss franc. Over the course of 2025, the dollar experienced a significant depreciation: the euro appreciated by 13.44%, while the dollar declined by 12.65% against the Swiss franc. Finally, Bitcoin fell 3.59% in December, with the crypto market remaining under pressure, particularly in the early part of the month. After reaching an all-time high in early October, Bitcoin corrected by approximately 30%, ending the year at USD 87,647.54 (–6.47% compared to 2024).

In December, the portfolio underperformed the benchmark. Fixed income performance was broadly in line, with mixed contributions across bond segments that did not materially affect overall results.

Equities were the primary source of underperformance. While the U.S. Small- and Mid-Cap ETF outperformed the S&P 500 Total Return Index following the Federal Reserve’s December rate cut, allocations to the Cybersecurity ETF, Amazon, and Microsoft weighed on performance. In Emerging Markets, the underweight to South Korea relative to the benchmark further detracted, as the market’s positive momentum continued. By contrast, diversification across Europe and Switzerland contributed positively.

Commodities and alternative investments partially offset equity-related weakness, supported by a strong rally in precious metals that boosted returns from the gold ETF and structured products linked to gold, silver, and gold miners.

On a year-to-date basis, while offering satisfying returns on an absolute level, the portfolios trailed the benchmark, with equities representing the main drag. A delayed allocation to Emerging Markets and an underweight to South Korea caused the portfolio to miss part of the region’s earlier gains. North American equities also underperformed, reflecting idiosyncratic weakness in Amazon and softer performance in small- and mid-cap stocks. The Hive equity fund, due to its conservative nature, was an additional detractor. These effects were partly offset by positive contributions from Swiss and broader European exposures, including structured products linked to the SMI.

Fixed income underperformance remained contained and was mainly driven by allocation effects in investment-grade and emerging market bonds. This was partially offset by outperformance in preferred shares and slightly higher duration within that segment.

Alternative investments detracted earlier in the year but improved toward year-end following the November allocation to a structured product linked to GLD and SLV. Commodities were a key source of outperformance for the year, led by sustained strength in gold and gold-mining exposures.

No major transactions were executed during December.

We wish you a great start to the new year!