Click Here to Download the PDF Version

“An eye for an eye only ends up making the whole world blind.” – Mahatma Gandhi, Indian Politician/Filosopher/Lawyer

ECONOMY: GEOPOLITICS IN THE WAY

Last time we updated you with our quarterly outlook, we presented a constructive view of the global economy. True, there were some areas of uncertainty—the labor market and the inflation outlook being the main ones, at least in the United States—but, honestly speaking, periods entirely devoid of economic uncertainty, even if mild, are very infrequent. Then came the war in Iran. Or perhaps, against Iran? It is no longer entirely clear which nuances to deploy when communicating in today’s complex and ambiguous world.

A lot has been said, more has been written, and even more has been speculated about the conflict in the Middle East, making any further comments from our end rather superfluous. As we write, and hopefully by the time you read this, a ceasefire has been declared (and is being respected) on multiple fronts; the USA–Israel duo has started truce talks with Iran, while Israel itself has also laid the groundwork for peace talks with Lebanon (a region heavily funded by Iranian capital and weaponry). Will it last? Who knows. Everything remains fragile, given that the demands of all parties involved are diametrically opposed. Yet, we like to believe that, notwithstanding the profound social and religious differences that characterize the parties involved and which led to the outbreak of the war, the majority of humankind—except for the fraction that is radical in its beliefs—does not, deep down, want war. Again, this reflects our hope rather than strict rationality.

Rationally speaking, the current U.S. administration needs a way out; midterm elections are on the horizon, and the domestic campaign will soon begin. History shows that entering elections with rising prices has often proven detrimental to the electoral outcomes. Yet, the impasse in the Middle East is a knotty problem. U.S. engagement in the region remains influenced by developments around the Strait of Hormuz, where disruptions to oil flows have contributed to higher energy prices. At the same time, resuming the conflict would risk triggering a fierce response from Iran, which, if cornered, may attack regional energy infrastructure—including its own—causing a severe and prolonged spike in energy prices. These are, of course, speculations; there are surely other solutions—if we knew them, we would be sitting in the Pentagon rather than in Switzerland making conjectures. However, what we do know is that the clock is ticking.

As we were saying, the global economy was in good shape—and still is. The effects of higher energy prices (WTI is in the low 90s $/barrel, off its recent peak but still well above the high 50s $/barrel pre-war), apart from at the gas pump where the reaction is immediate, have only started to come through in recent weeks. It will take several months before higher energy prices fully feed through to the rest of the economy. Should this occur, the global economic outlook could change materially.

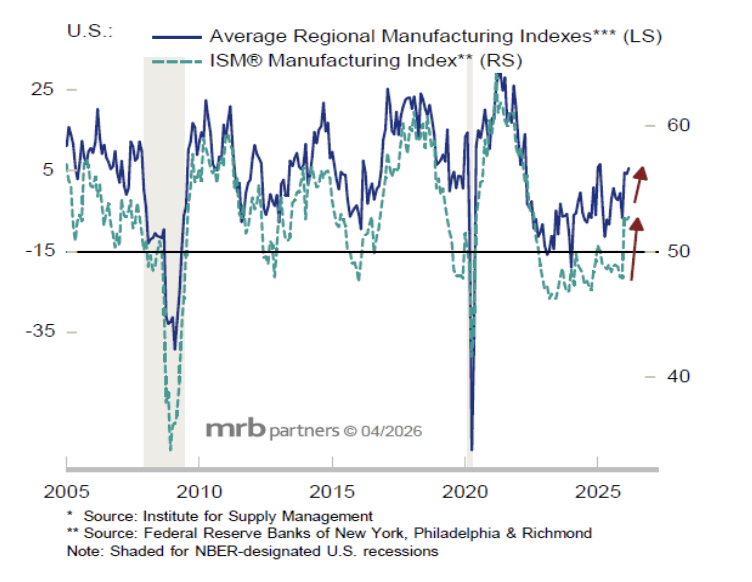

Energy sits at the epicenter of most production processes; higher energy costs translate into higher prices across a vast range of products—from food to fertilizers, from medicines to construction materials. Thus, it is of paramount importance that energy prices normalize soon. Fortunately, the resilience of the U.S. economy has been remarkable, and only a shock could materially weaken it. Manufacturing is improving, as shown by various leading indicators picking up pace and now in expansion territory. It seems we may be past the inflection point; the Federal Reserve (Fed) is on hold, which should be stimulative for the U.S. economy, and many manufacturers have passed through a large part of the tariff-induced price increase (which, in the meantime, has been partially rolled back by a Federal Court). The services sector, on the other hand, has slowed in recent months, but remains above the contraction threshold; therefore, recession probabilities remain in the low to mid-single digits, according to several econometric models, including our own—this, of course, prior to the rise in energy prices.

The Federal Court’s decision to partially reverse part of the tariffs imposed by the current administration offers an olive branch to the U.S. consumer, as it helps offset part of the drag coming from rising costs stemming from the conflict in the Middle East. This should help support the American consumer, who has remained very resilient throughout the various shocks—higher interest rates, tariffs, and now turmoil in energy markets—that have hit the U.S. economy over the last few years. We anticipate that the median household will spend in line with income growth, which is currently normalizing toward a non-inflationary level of 3.5%–4.0%. The top income quintile, representing 40% of discretionary spending, is doing well, but how much pent-up demand remains is uncertain—likely not much, in our view. Banks’ willingness to lend, alongside a lighter regulatory burden, is improving, providing an additional positive. Similarly, the wealth effect continues to support those who have sufficient assets to gain exposure to financial markets which, despite periods of volatility, have generally trended upward in recent years and may continue to support household balance sheets.

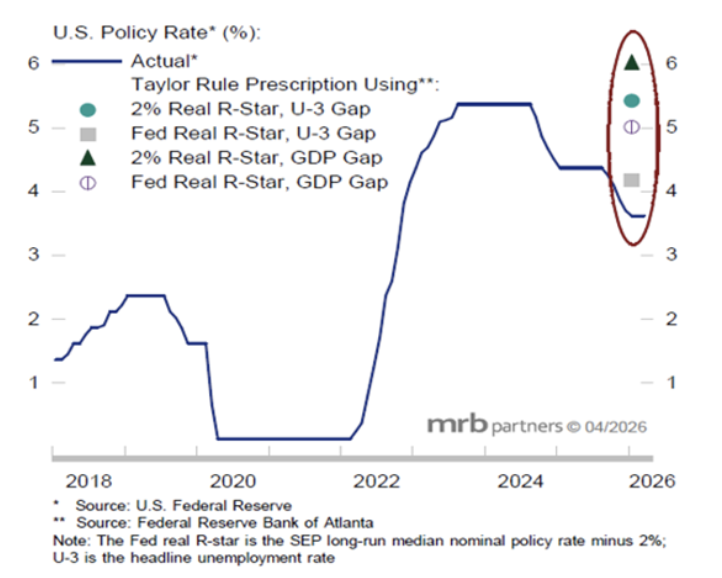

The labor market and inflation—two aspects that have concerned us in recent quarters—appear to be relatively contained (more the former than the latter). JOLTS data have normalized at lower levels for this cycle, but these levels still correspond to the upper range of previous cycles, suggesting a relatively solid labor market; as long as corporate margins and deficit spending remain elevated, job cuts are likely to be delayed. Inflation, on the other hand, could move back above 3.0%, exceeding the Fed’s target. Higher capital goods prices and oil are the main drivers. The increasing budget deficit and a positive output gap are also likely exerting upward pressure. The new Fed Chair will face a complex task, in our view. Rates are expected to remain elevated relative to the state of the economy. A resolution to the conflict in the Middle East could help alleviate these pressures. However, for the moment, investors do not believe long-term inflation will rise as much as Main Street expects; long-term expectations have remained fairly anchored to recent averages, while short-term expectations have closely mirrored the rise in oil prices.

The weaker spot now appears to be the housing market, as affordability issues persist. On the one hand, the combination of stable to mildly declining prices and stable long-term rates supports housing activity, albeit at low levels, leading to improving inventories. On the other hand, declining prices may weigh on activity, with multi-family housing and commercial real estate remaining the most problematic segments—particularly for regional banks, though less so for households.

To put it all together, the conflict in the Middle East is contributing to higher recession risks, but the starting point remains solid, and it would take a meaningful shock for the U.S. economy to falter. The partial reversal of tariffs should help ease the burden of higher energy prices, and the Fed’s stance will remain accommodative, even as it avoids further rate cuts, given that real rates are currently close to zero.

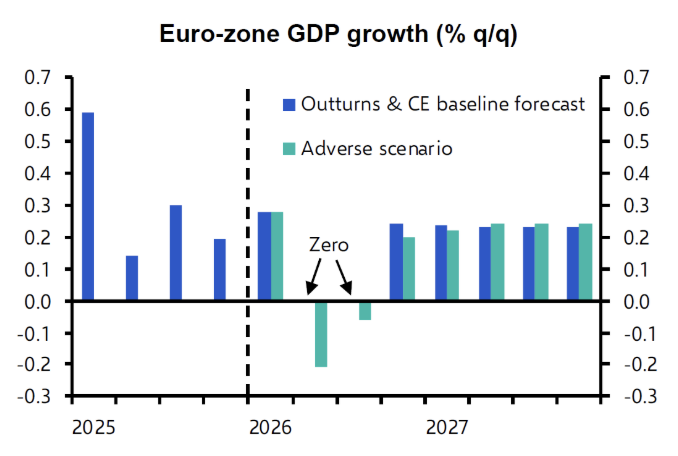

The U.S.’ main economic counterparts—Europe and China—are experiencing a slowdown in economic activity, albeit for different reasons. Europe’s industry-focused economy is highly energy-intensive, as evidenced in the aftermath of Russia’s invasion of Ukraine. High energy prices are far more impactful here than in other developed economies, particularly because alternatives are in short supply; the risk of an oil shock-induced slowdown is real. Growth expectations have deteriorated in recent months, with economists now predicting stagnation for the next few quarters. Wage growth remains resilient, supported by the services sector, and we expect inflation to pick up in the near term, potentially forcing the ECB to act pre-emptively, reversing our previous expectations for a more dovish stance. However, visibility remains low, and the level of confidence we attach to this—or any—scenario is currently limited.

The other ailing party, China, has successfully replaced the U.S. with Europe and the rest of the world as the primary destination for its exports. Strong exports are sustaining growth and maintaining a positive trade balance. Yet, a 3% GDP growth rate is nowhere near the initial target. It appears that China has reached stall speed. The Chinese consumer remains in good shape, with a high savings rate. However, domestic consumption remains constrained, as the country continues to work through a balance sheet recession, much of which is linked to housing, representing approximately 70% of total savings. Moreover, government revenues are under pressure due to the ongoing real estate crisis, while debt-to-GDP levels remain high, forcing a retrenchment in fiscal spending. On the positive side, the fact that most government debt is held domestically should help reduce the risk of a systemic financial event. Taken together, the situation leaves room for improvement, but ongoing domestic and external complexities leave limited room for policy errors.

FIXED INCOME: DON’T BE GREEDY

There are two key messages we wish to convey. Long-term rates remain vulnerable, and investment-grade bonds continue to represent the most attractive asset class on a relative basis.

Fiscal imbalances, political instability, mounting inflation pressures, and rising debt ratios leave long-term rates exposed, at least over the next twelve months. Even beyond the war, the combination of a positive output gap and accommodative monetary and fiscal policies increases the risk of higher inflation. Admittedly, as outlined earlier, long-term inflation expectations have not become unanchored, which is encouraging. But why take unnecessary risks? In this environment, maintaining a conservative duration stance—or hedging long-duration exposure—appears both necessary and warranted.

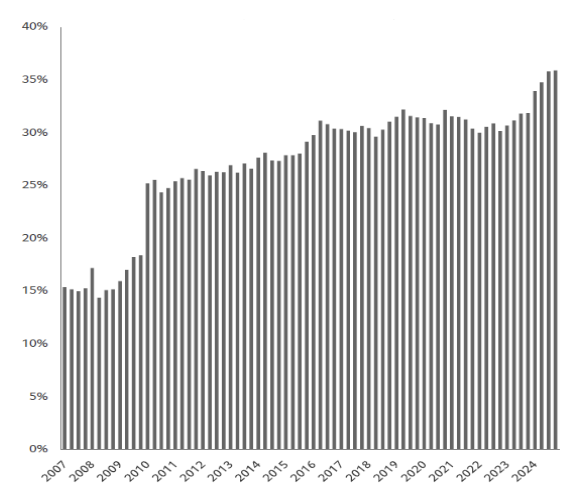

Investment-grade bonds continue to offer solid fundamentals and compelling yields. U.S. EBITDA margins are near two-decade highs, while yields have only been higher during the bond sell-off of 2022. Rating trends remain supportive, with upgrades consistently outnumbering downgrades. The weak point, unsurprisingly, is valuation. Assets appear broadly expensive—not just within fixed income—and investment-grade bonds are no exception, with spreads to risk-free assets near historical lows. However, on a relative basis, the segment still offers attractive opportunities.

This remains true relative to high yield, emerging markets, and subordinated debt. High yield appears particularly vulnerable, as fundamentals are deteriorating. Downgrades remain elevated and exceed upgrades. Default rates are under control, which is positive, but spreads are very tight, making exposure more sensitive to a constructive economic outlook. A similar conclusion applies to emerging markets and subordinated debt: fundamentals remain solid, but valuations are stretched both in absolute and relative terms. Valuations do not trigger market corrections—but they amplify them when they occur.

EQUITY: WILL HIGH ENERGY PRICES DERAIL THE BULL MARKET?

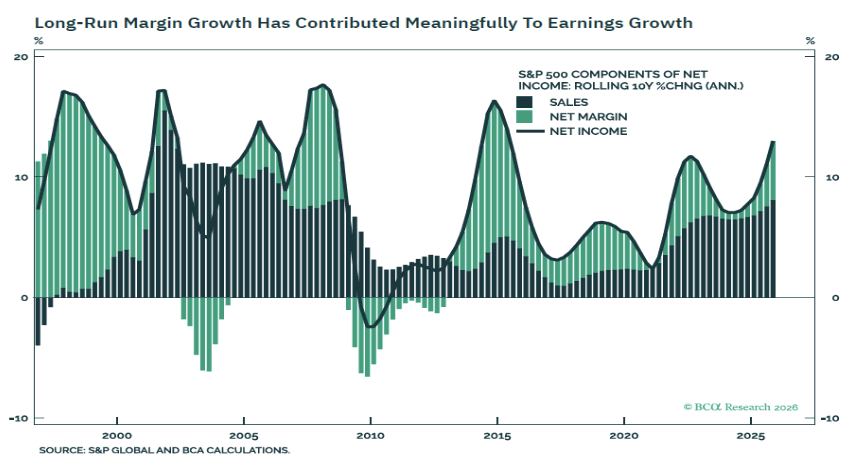

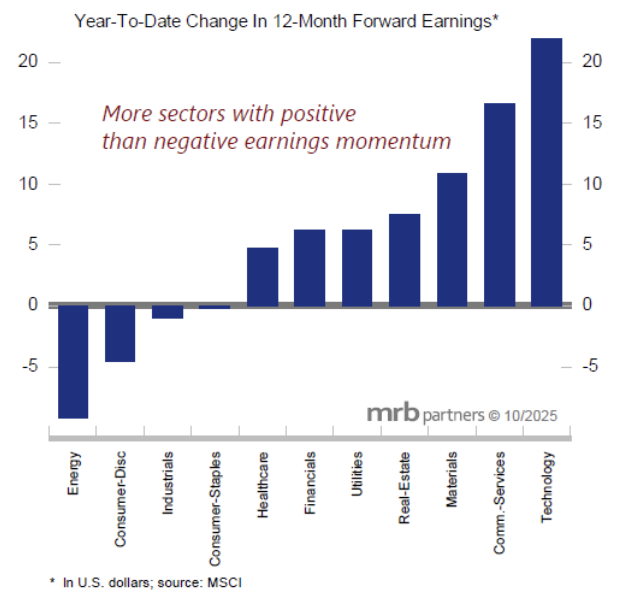

If we assume that the current energy shock will not be sufficient to trigger a recession, we believe equity prices will grow broadly in line with earnings. Speaking of which, the strong momentum is likely to continue into 2026. Technology and Media remain the primary drivers of growth, but earnings breadth is improving, supporting the widely held view that we may be on the cusp of a new commodity and real asset cycle. The spillover effects of A.I., particularly in utilities and industrials, are also becoming evident, as hyperscalers show little intention of slowing the investment cycle initiated a few years ago—especially now that some companies have started to monetize these investments. We believe capital expenditure will remain strong, supported by robust demand for A.I.-related products and solid balance sheets—cash levels remain elevated, albeit off their peaks, while debt levels are low and easily serviceable, given that much of it was refinanced during the COVID period at near-zero interest rates.

While earnings growth is becoming broader, we still see the Technology sector as remaining at the center of both earnings growth and margin expansion. As a result, the market remains highly concentrated from both a return and earnings perspective; between 60% and 70% of earnings growth is generated by the Technology and Media sectors. This dominance represents both a strength and a risk. As goes tech, so goes the market. Provided that the A.I. theme remains intact, returns should remain supported. At this stage, we see few reasons for the trend to reverse in the near term; incremental profit margins in these sectors approach 50%, compared with roughly 10% for the rest of the market.

Such an attractive profile partially justifies the elevated valuations that currently characterize the equity market. Admittedly, high valuations represent a headwind for long-term returns, although they are not, as we have often noted, a catalyst for an outright correction. The forward multiple has recently declined, supported by strong EPS growth. The S&P 500 is currently pricing in approximately 400 basis points of earnings growth above nominal GDP growth—a reasonable assumption if margins hold and no recession materializes. At the same time, market-implied valuations suggest a low single-digit probability of recession over the next twelve months, with real yields at around 1.5% (currently lower) and an equilibrium rate of roughly 4% (also below current levels). In summary, equities should continue to grow broadly in line with earnings trends, driven primarily by Technology and Media and supported by secondary sectors such as industrials and utilities. Elevated valuations, however, remain a Sword of Damocles on long-term returns.

A brief note on non-U.S. markets. European companies are expected to benefit from a broadening recovery in earnings growth, supported by cost-cutting measures and potentially lower wage pressures. However, rising energy costs represent a significant tail risk for the region at this stage. Services-led economies such as Italy and Spain have helped offset the weakness in more capital-intensive countries such as Germany and France. Looking ahead, increased infrastructure and defence spending may partially reverse this dynamic. From a valuation standpoint, Europe’s discount has narrowed and, given the higher recession risk and structurally lower growth profile (notably due to limited Technology exposure), the remaining discount appears justified.

Emerging markets, by contrast, may continue to benefit from a further weakening of the U.S. dollar. Selectivity remains key, as not all markets are likely to move in unison, but a weaker dollar tends to favour export-oriented economies and helps contain debt burdens. Avoiding highly concentrated indices, such as the Kospi, or particularly expensive markets, also appears to be a reasonable approach.

CURRENCIES AND COMMODITIES: LONG-TERM VIEWS UNALTERED

In previous commentaries, we outlined how the abundant supply of oil, combined with stable demand, would have capped prices. Barring geopolitical risks. This was as much a cliché as it was true. We have already extensively discussed the conflict in the Middle East and will therefore not dwell further on the topic. As long as the Strait of Hormuz remains closed and/or under Iranian control, energy prices will struggle to recede. However, should the situation normalize, we believe prices could decline, with a caveat related to the damage inflicted on regional refineries, which may keep global oil supply partially constrained even if vessel flows through the Strait return to normal.

When discussing gold—the yellow metal—we are often told that it serves as a hedge against geopolitical risks, acting as a safe-haven asset. We have consistently challenged this view, as historical evidence suggests that gold prices do not exhibit a stable correlation with geopolitical shocks, but are instead more closely driven by movements in the U.S. dollar and real interest rates. The recent conflict is yet another example: gold prices moved from a peak of nearly 5,500 $/oz. to a low of 4,100 $/oz. within a matter of weeks. Rising real rates and a stronger USD were the primary drivers of this decline. As we write, gold has rebounded to around 4,700 $/oz., roughly midway through the previous drawdown. Our view on gold remains unchanged and is tied to our expectations for the USD and real rates. Given our outlook for a weaker dollar in the medium term—pressured by rising fiscal deficits, increasing public debt, and sticky inflation—we remain constructive on gold.

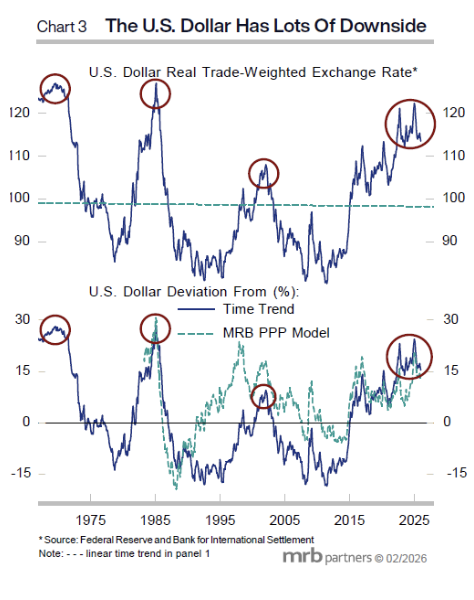

Alternatives to the USD—which is close to pre-conflict lows and still estimated to be overvalued by roughly 20%—can be found in regions with stronger balance sheets, such as Europe and Switzerland, or in economies with higher growth potential, such as selected emerging markets. Moreover, if one subscribes to the view that we are at the cusp of a new commodity super-cycle, it makes sense to focus on currencies of countries that rely heavily on raw material exports, as they stand to benefit. The Australian dollar, to cite just one example, fits this profile well.

OUR STANCE:

Disclaimer

This investment report prepared by Lugano Financial Advisors SA (“LFA”), contains selected information and investment opportunities identified by LFA. This document is based on sources believed to be and reliable, accurate and complete. In particular, LFA shall not be liable for the accuracy and completeness of the statements estimates and conclusions derived from the information contained in this document. Any information in this document is purely indicative. This document is not a contractual document and/or any form of recommendation. It does not constitute an offer, a solicitation, advice, or recommendation to purchase, subscribe for or sell any financial instruments. Under no circumstances, LFA shall be liable for any kind of damages, direct, indirect, or non-contractual. Prices and rates indicated are subject to change without prior notice. The investments are valued at the market price as of the investment reporting date (e.g. stock exchange closing price, Net asset value or market maker price). Should no market price be available as of the investment reporting date, LFA shall use the last available price for the valuation. LFA shall assume no obligation to purchase or sell the investments at the reported market prices. The data provided in this investment report, which do not specifically refer to the account and custody account positions of the client, are intended solely for the client’s own use and may not be passed on or used independently of the client-related data stated in this investment reporting. Reliance on the data contained in this investment report and any resulting act or omission on the part of the client or third parties shall be at the client’s or third party’s own risk. Past performance should not be seen as an indication of future performance. This investment report is not intended to be used for tax purposes. Please check this investment report and inform LFA of any discrepancies within 4 weeks.