2026/July

“A good parent protects their child.

A good parent lets their child face risk.

Two truths that can be managed with context, analysis and balance.”

ECONOMY: TWO TRUTHS, ONE PORTFOLIO

At times the market looks split in two. Macro investors look at sticky inflation, elevated fiscal deficits, higher long-term yields and geopolitical fragility, and conclude that caution is warranted. Bottom-up investors look at earnings revisions, AI-related capital expenditure, strong corporate margins and resilient consumption, and conclude that risk assets still deserve a place in portfolios.

The economy is not fragile enough to justify an aggressive retreat from markets, but valuations and leverage make it less forgiving than it looked a few months ago. The correct response is therefore not to abandon market exposure; it is to reduce the risks that are least well paid and to add shock absorbers where the cost of protection is still reasonable.

The United States remains the center of gravity. Activity is supported by capex, particularly in software, equipment and data infrastructure. The important nuance is concentration: when a large share of incremental growth comes from a narrow investment boom, the cycle becomes more dependent on the willingness of hyperscalers – the largest cloud-computing providers – to keep spending and on the ability of the power grid and supply chains to keep up.

Europe is improving from a low base, helped by services in the periphery and by infrastructure and defense plans in the core. Yet the region remains the weak link during an energy shock because its industrial base is more energy-intensive and its equity market has less exposure to the technology sectors that dominate global earnings growth. China, meanwhile, continues to rely heavily on exports, while domestic demand remains constrained by a housing-linked balance-sheet recession, in which households and companies focus on repaying debt rather than on new spending.

What many investors may be underestimating

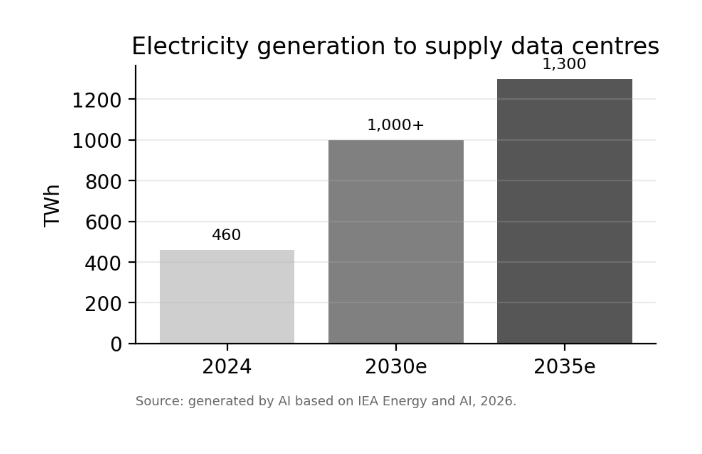

• AI is not only a software story. It is becoming a power, grid, cooling, copper and financing story.

• The key constraint may shift from demand for AI services to the availability and cost of physical infrastructure.

• This supports selected AI beneficiaries, utilities, grid infrastructure and copper-linked assets, but it also increases execution risk for the most crowded mega-cap trades.

EQUITIES: REAL EARNINGS, CROWDED POSITIONING

The earnings backdrop remains supportive. S&P 500 earnings growth was strong in Q1, broad across sectors, and still led by technology and communication services. This matters: the AI story is no longer only a narrative about future productivity. It is already visible in capex, infrastructure orders and earnings revisions.

The uncomfortable part is that the same facts that justify staying invested also explain why the market is crowded. The largest technology and media companies continue to account for a disproportionate share of margin expansion and earnings growth. When technology leads, the market follows. That is a strength when the AI investment cycle works; it is a vulnerability when expectations leave little room for disappointment.

Our conclusion is selective exposure. We would reduce broad U.S. equity beta (sensitivity to overall market movements), avoid chasing momentum indiscriminately and keep exposure to quality companies that can convert AI spending into durable cash flows. The volatility index (VIX) is very low, but a calm index can conceal fragile positioning beneath the surface.

The risk is not that AI is fake. The risk is that the market may have priced too much of the good news into too few balance sheets.

FIXED INCOME: ADD QUALITY, NOT CREDIT BETA

Fixed income is again investable, but not all carry (the income earned from simply holding an asset) is equally attractive. Absolute yields remain appealing, while credit spreads – the extra yield corporate bonds offer over government bonds – are tight and therefore less able to absorb negative surprises. In this environment, creditworthiness is more valuable than reaching for the last few basis points of spread.

The portfolio action is straightforward: increase investment grade and intermediate-duration government exposure. The intermediate segment of the curve should also be better insulated from the forces that may push long-term rates higher. This improves the portfolio’s ability to withstand a growth scare without making an aggressive duration bet at the long end of the curve.

The main macroeconomic risk is not a classic recession today. It is a sudden and prolonged rise in long-term yields caused by the wrong mix of fiscal stimulus, monetary accommodation and persistent inflation. That risk argues for discipline on duration (the portfolio’s sensitivity to interest-rate moves), but also for owning high-quality assets that would perform better if growth slowed abruptly.

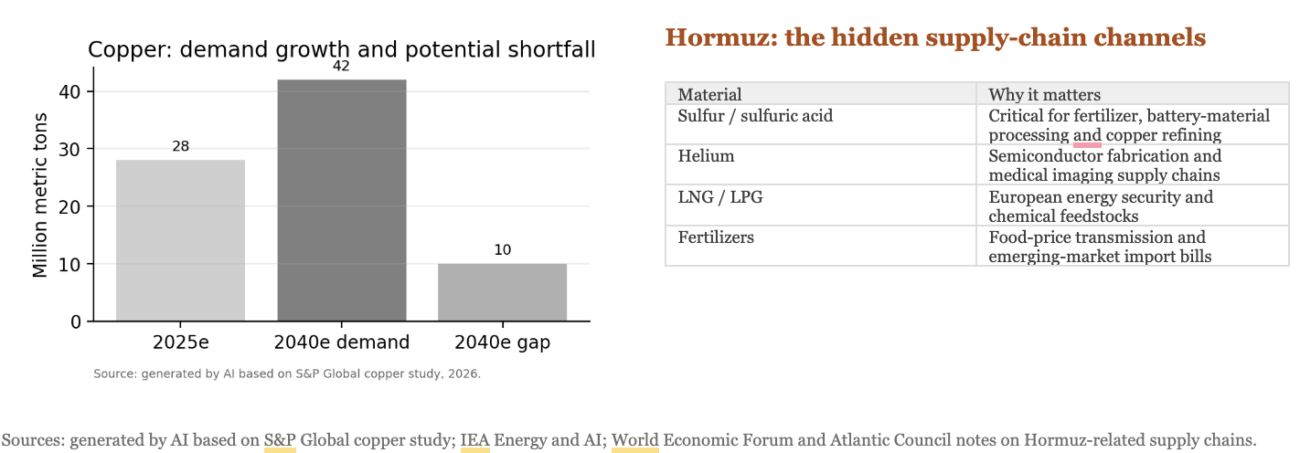

COMMODITIES: NOT ONLY HORMUZ, NOT ONLY OIL

The market naturally focuses on oil when the Strait of Hormuz is at the center of geopolitical risk. That is correct, but incomplete. Beyond the crisis in Iran, further flashpoints could emerge around the world, driven by the long-term strategic rivalry between China and the United States over economic and political leadership. This competition for critical materials is also relevant for LNG, fertilizers, sulfur, helium, LPG and chemicals – inputs that sit inside food, semiconductor, battery, healthcare and industrial supply chains.

This is why an energy shock should not be analyzed only as a gasoline-price story. If disruption persists, the second-round effects may arrive through fertilizer prices, food inflation, chemical feedstocks and semiconductor supply chains. The first signal worth monitoring is therefore not only crude oil, but also producer-price pressure in food and industrial inputs.

We continue to view gold as a strategic hedge against deficits, geopolitics and confidence shocks. However, a portfolio that hedges only through gold may be too concentrated in one real asset. Copper offers a different type of hedge: it is tied to the physical bottlenecks of electrification, AI infrastructure and grid investment.

CONCLUSION: CONSTRUCTIVE, BUT LESS FORGIVING

The market is not obviously wrong. Growth is still positive, corporate earnings are strong, AI investment is real and the global cycle is not yet recessionary. But the market is also not cheap, not broad enough and not immune to an abrupt repricing in rates, inflation, leverage or geopolitical risk.

Our stance is mildly constructive. The right portfolio today should preserve upside participation, reduce risks that bear little reward, and diversify shock absorbers. In short: keep the engine running but improve the brakes.

OUR STANCE

CONTACT US

DISCLAIMER

This document has been prepared by Lugano Financial Advisors SA (LFA) for information purposes only. It is based on sources believed to be reliable and on internal analysis, but no representation is made as to the accuracy or completeness of the information, estimates or conclusions contained herein.

The document does not constitute an offer, solicitation, advice or recommendation to buy, sell or subscribe for any financial instrument. Prices, valuations and market views are subject to change without notice. Past performance is not indicative of future results. Investors should consider their own financial situation, risk tolerance and investment objectives before making any investment decision.