- AI and Inflation are driving the markets

- Economic Growth and Corporates are healthy

- Interest rates are the key variable for the sustainability of the current trends

The Battle Between Inflation and Artificial Intelligence

The key themes we highlighted in April remain largely unchanged. Markets continue to be driven by the tension between increasingly challenging macroeconomic conditions and exceptionally strong microeconomic developments.

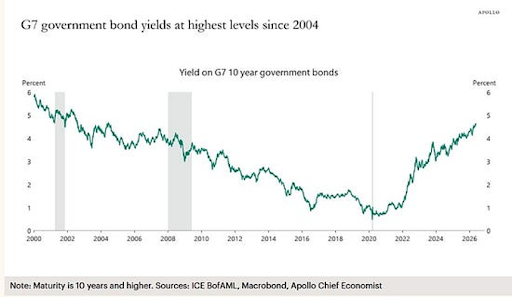

On the macro side, the energy shock resulting from the potential disruption of oil flows through the Strait of Hormuz risks becoming a more persistent source of global inflation in the coming months. So far, the impact has been limited to energy prices, but if sustained, it could gradually spread to other components of the inflation basket. This could interrupt the rate-cutting cycle currently anticipated by central banks and reinforce the view that the economic cycle is entering a more mature phase.

At the same time, corporate fundamentals – particularly within the AI ecosystem – remain solid, as reflected in recent earnings and capital expenditure data. Earnings growth, margins, capital expenditure, financing activity, and investor flows continue to be concentrated around companies exposed to artificial intelligence. Semiconductors, data centers, digital infrastructure, energy suppliers, industrial automation and select real estate segments have emerged as the primary beneficiaries of this investment cycle. Artificial intelligence is no longer a distant promise; it is already reshaping corporate spending and business models across industries.

However, elevated valuations in AI-related sectors remain vulnerable to shifts in sentiment, competitive dynamics, or delays in monetization.

This leaves investors facing a crucial question: are current valuations justified by future earnings growth, or has enthusiasm moved ahead of fundamentals? The answer becomes increasingly important as markets prepare to absorb a potentially unprecedented wave of new listings, including names such as SpaceX, OpenAI, Anthropic, Databricks, Canva and Stripe, that will be one of the topics of the June commentary.

The clashing point between these two forces – higher inflation and explosive AI-driven growth – will likely be determined by interest rates. If inflation pressures lead to higher funding costs and wider corporate credit spreads, the economics of the massive investments currently being made in AI infrastructure may come under greater scrutiny, mainly for low quality, highly leveraged companies. Conversely, if energy markets stabilize and inflation expectations remain anchored, the current investment cycle could prove more durable than many investors expect.

For this reason, the reopening of the Strait of Hormuz and economic growth indicators remain important variables to monitor. Their impact extends well beyond oil prices, influencing inflation expectations, monetary policy and ultimately the sustainability of today’s elevated market valuations.

Markets

May was characterized by a mix of both positive and negative factors, which nevertheless did not undermine equity investors’ confidence.

Equities

The main global indices continued the upward trend that began in April. Among the supportive elements were reported expectations of a peace agreement between the United States and Iran, strong earnings from companies operating in the artificial intelligence sector, and the U.S. labor market, which in April showed stronger-than-expected growth. On the downside, rising inflation driven by energy prices, higher long-term U.S. Treasury yields, and some concerns about the resilience of American consumers weighed on sentiment. At the sector level, performance was once again driven by AI-related industries, while Utilities and Energy underperformed following the correction in oil prices.

Fixed Income

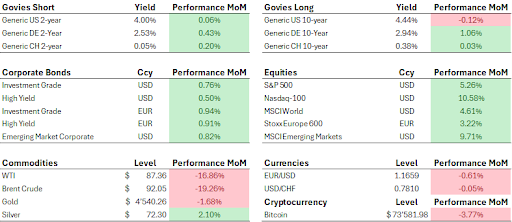

In the bond market, government yield trends were mixed. In the United States, yields rose compared with the previous month, despite expectations of a possible peace agreement in the Middle East. In Germany and Switzerland, 10-year yields initially followed a similar trend, but then closed at lower levels than at the end of April. On the short end of the curve, movements were consistent with those on the long end. On the credit side, despite significant rate volatility, particularly in the United States, the investment grade segment posted positive performance both in Europe and the U.S. The high yield segment also ended the month in positive territory. Emerging market bonds also delivered positive performance.

Commodities

In the commodities market, May was marked by high volatility. In this context, both WTI and Brent corrected significantly from their monthly highs, closing around USD 90 per barrel as of May 31, 2026. Gold ended the month lower, weighed down by higher-than-expected inflation data.

Currencies

In the currency market, the U.S. dollar gained ground against the Euro, supported by inflation expectations and the possibility of a more restrictive monetary policy by the Fed. Against the Swiss franc, the exchange rate closed the month broadly unchanged. Lastly, Bitcoin reversed the previous month’s trend, closing in negative territory.

Source: Bloomberg LP, as at 31 May 2026

Performance Commentary

In May, portfolio activity remained broadly stable, with positioning maintained in line with the strategy’s investment framework.

The fixed income allocation ended the period with a slight positive contribution after recording losses around mid-month. However, the subsequent decline in yields supported a recovery in bond prices, allowing the asset class to close the month with positive returns across its main segments.

Equities were the main driver of performance, with North America accounting for the largest share of gains. The portfolio’s exposure to US cybersecurity and software companies contributed positively to relative performance, as earnings reports highlighted solid fundamentals and resilient business models. This helped confirm that part of the market weakness experienced in previous months had been excessive. The broader US equity market also posted a positive return during the period, providing further support to portfolio performance. Lastly, both Emerging Markets and the global diversification allocation contributed positively once again.

Alternative Investments also made a positive contribution to performance, notwithstanding the ongoing correction in private equity markets since the beginning of the year.

By contrast, commodities were the only detractor in absolute terms, mainly due to volatility in gold prices. Rising bond yields encouraged investors to rotate towards yield-bearing assets and away from non-yielding assets such as gold.

While May results were broadly positive across asset classes, material risks remain that could affect future performance. Persistent energy price pressures and elevated long-term yields may weigh on both fixed income and equity valuations in the coming months. AI-related sectors, which were the primary driver of equity gains, remain exposed to sentiment shifts, monetisation delays and increasing competitive dynamics. Additionally, uncertainty surrounding the path of monetary policy continues to represent a key variable for portfolio returns. Market and index performance data referenced throughout this commentary are sourced from ICE BofAML, Macrobond, Apollo Chief Economist, Bloomberg LP and are provided for informational purposes only. They do not represent the performance of any portfolio managed by LFA.

Transactions

No transactions took place over the period.

Disclaimer This material is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Past performance does not guarantee future results, and all investments involve risk, including potential loss of capital. Any forward-looking statements are inherently uncertain and subject to change. References to specific securities are for attribution only and should not be construed as a recommendation. Third-party data are believed to be reliable but are not guaranteed and may change without notice.