• AI, Oil and Interest Rates drove markets in June

• Growth remained resilient in June

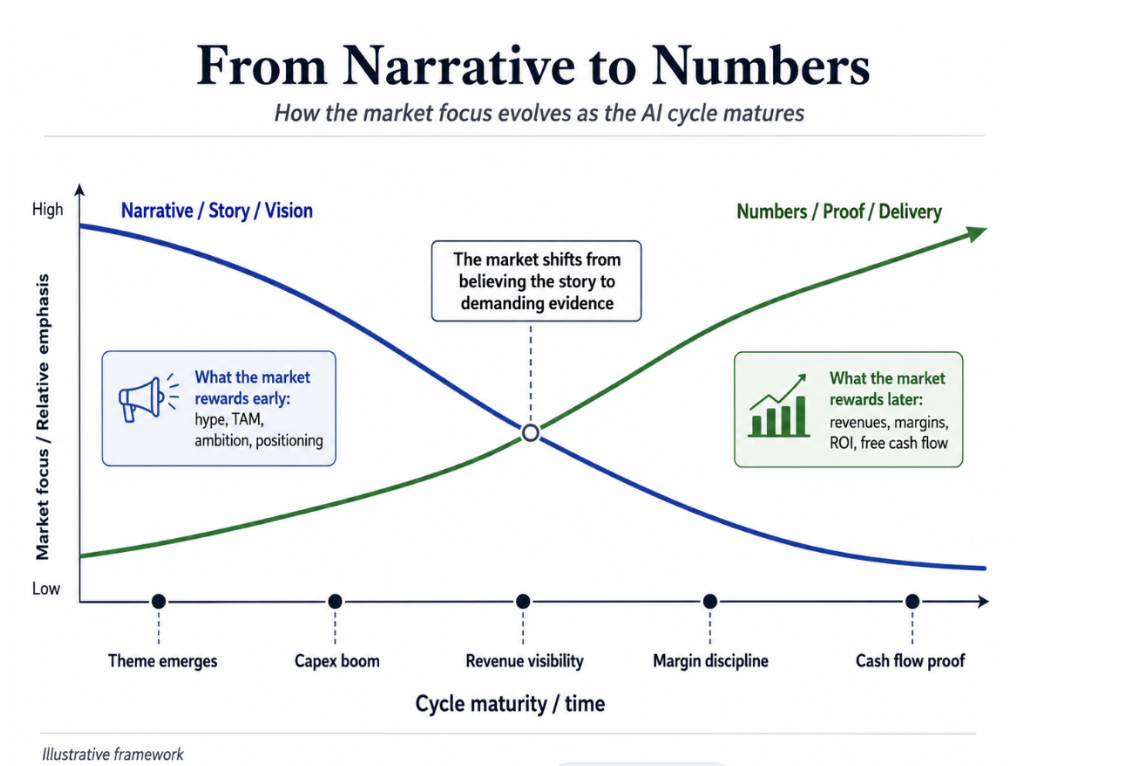

• AI-related investment themes continue to evolve as companies increasingly report commercial deployment and financial results associated with AI initiatives

From Oil Shock to AI Execution

June was a month of reversals. At the beginning of the month, markets were still focused on three risks: stronger economic data, higher oil prices, and the possibility that central banks would be forced to remain restrictive for longer. The U.S. jobs report released early in the month triggered a sharp risk-off move, as investors increased expectations of a more hawkish Federal Reserve. Equity markets weakened, technology shares came under pressure and the focus moved back to interest rates.

The pressure driven by tensions around Iran and the Strait of Hormuz eased materially in the second half of the month, as hopes of a U.S.-Iran agreement increased and oil prices fell by more than 5% in a single session. Market pricing suggested that investors viewed the geopolitical risks as less likely to result in a sustained inflationary event. Central banks remained cautious. The Fed left rates unchanged at 3.50–3.75%, describing economic activity as expanding at a solid pace, with strong productivity and capital investment, but inflation still elevated relative to its 2% target. In Europe, the ECB raised rates by 25 basis points and revised inflation projections higher for 2026 and 2027, mainly because of the higher path for energy prices.

On the corporate side, artificial intelligence remained an important investment theme, but June also showed the first signs of a more demanding market. Semiconductors, memory, data centers, power infrastructure, grid equipment, and cooling systems generally benefited from continued investment activity during the period. At the same time, investors started to question the cost and funding of AI capex, especially where spending is debt-funded or where the future return is still unclear. This became visible in the second half of the month. On 23 June, the Nasdaq and the S&P 500 fell, dragged down by a sharp sell-off in semiconductors. The Philadelphia Semiconductor Index dropped 7.9%, while the S&P 500 technology sector fell 3.7%. This was an important change in tone: AI was still the market’s strongest structural theme, but not every AI-related stock was treated as untouchable. Investors increasingly appear to be evaluating AI-related companies based on reported financial results and execution rather than longer-term expectations alone. Market performance increasingly reflects company-specific execution and financial results in addition to broader investment narratives. It is starting to distinguish between companies writing the checks and companies receiving them. Hyperscalers are investing heavily, while semiconductors, memory, power equipment, and infrastructure suppliers have generally benefited from increased spending associated with AI infrastructure investment.

The conclusion for June is therefore more factual than dramatic. Growth remained relatively resilient during the period, many companies continued to report generally healthy corporate fundamentals, and AI-related companies continued to represent an important driver of market performance, although in a broader market performance. But future market developments may continue to be influenced by the same variable: interest rates. If inflation remains contained and funding costs stay under control the investment cycle may continue. If inflation reaccelerates and the cost of capital rises, markets may become more selective.

Source: AI-assisted illustration created using Claude (Anthropic).

Market Performance

Markets

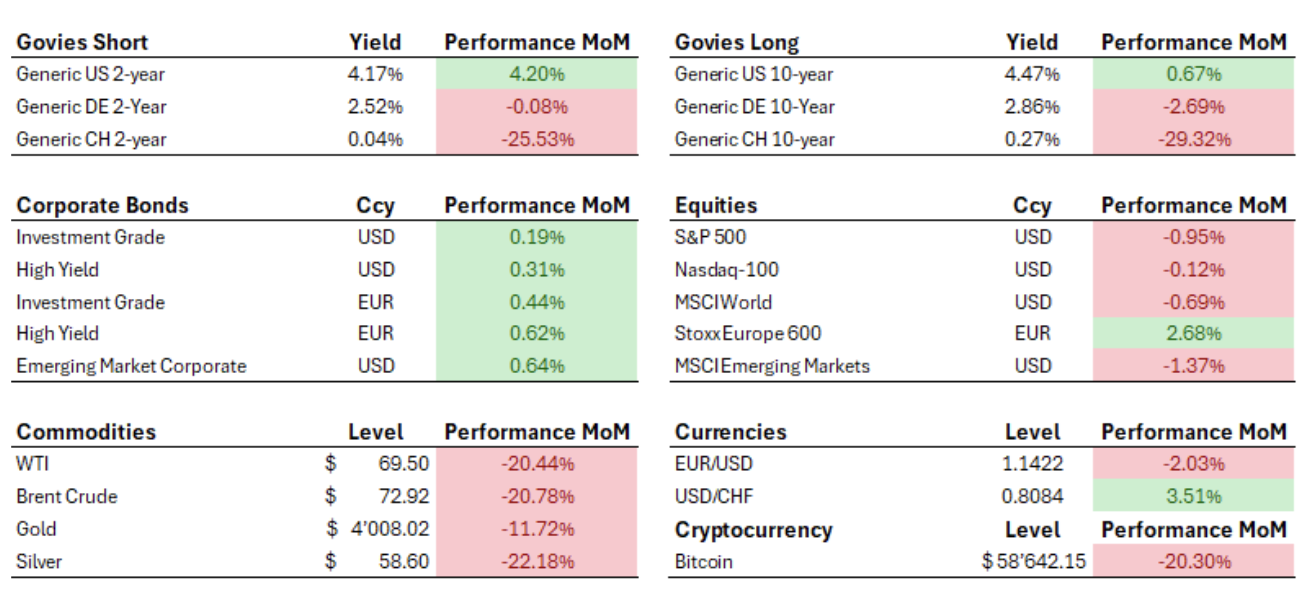

Financial markets ended June with generally improved investor sentiment after a volatile first half of the month. European equities outperformed U.S. markets, government bond yields diverged across regions, and commodities retraced most of their geopolitical risk premium as investor sentiment gradually improved.

Equities

Equity market performance was mixed across regions. European indices outperformed, supported by financials and defensive sectors, while U.S. equities experienced a period of consolidation following earlier gains during the year. Emerging Markets ended the month slightly lower, mainly reflecting weakness in Asian technology stocks.

Fixed Income

Government bond markets diverged. U.S. Treasury yields moved higher, while German Bunds and Swiss government bonds rallied as yields declined. Credit markets remained resilient, with both investment grade and high yield corporate bonds delivering positive returns despite elevated market volatility.

Commodities

Oil prices gave back most of their earlier gains, ending the month close to pre-conflict levels. Precious metals also weakened as safe-haven demand faded, with both gold and silver posting negative monthly returns.

Currencies

The U.S. dollar strengthened against both the euro and the Swiss franc. Bitcoin also declined significantly, falling by more than 20% as investors reduced exposure to higher-risk assets.

Source: Bloomberg LP, as at 30 June 2026

Performance Commentary

Past performance is not indicative of future results. Portfolio returns discussed below are presented solely for informational purposes.

In June, the portfolio experienced a negative return for the period, as most asset classes contributed negatively. Fixed income was the only neutral component, while equities, commodities and alternative investments weighed on performance.

Fixed income ended the month flat, supported by a stabilization in bond markets after the volatility experienced in previous weeks. The asset class avoided material negative contributions across its main sleeves.

Equities were the main source of weakness. After the strong recovery recorded during the second quarter, markets entered a consolidation phase in June, with pressure concentrated primarily in technology and AI-related stocks.

Alternative Investments also had a negative impact, mainly due to continued pressure on less liquid strategies. Private equity continued to decline from earlier in the year, while hedge fund exposure remained more defensive and generated a positive contribution, although not enough to offset weakness elsewhere.

Commodities also weighed on results, driven by the reversal in energy and gold prices during the month.

Transactions

No material transactions were made to the model portfolio during the period.

Disclaimer This material is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Past performance does not guarantee future results, and all investments involve risk, including potential loss of capital. Any forward-looking statements are inherently uncertain and subject to change. References to specific securities are for attribution only and should not be construed as a recommendation. Third-party data are believed to be reliable but are not guaranteed and may change without notice.