“It takes 20 years to build a reputation and five minutes to ruin it.” – Warren Buffett, Investor

ECONOMY: THE SPECTRE BACK IN THE CLOSET?

What a week! I must be honest; at one point I was skeptical about even writing our usual quarterly update. If Goldman Sachs changes its economic view within an hour, moving from recession to no recession in a matter of minutes and solely based on a tweet from the President, how can anything we write remain valid for more than a weekend?! (To be fair to Goldman Sachs, the imposition of tariffs or their removal does make a significant difference in how the global economy will unfold during the year.)

Speaking of tariffs and tweets, it’s time we suffer some self-inflicted irony. So much for “(…) history shows a new president has very little influence on either (financial markets or the economy)”. This is what we wrote back in November, the day after President Trump was elected for his second term at the White House. No phrase was ever more wrong! While his tariffs, and methods, were well-known and largely expected, most of us were caught off guard by the extent of the Trumpism found in both, which led to the increased (euphemism) volatility in financial markets.

However, it’s worth noting that a few weeks later we published November’s market commentary, titled Facing Four Years of Tweet-Related Volatility.

We acknowledge that we don’t have President Trump’s influence, as well as his global reach but, those of you who have followed our words, in a similar fashion as how investors recently flocked into the equity markets because of Trump’s recent “This is a great time to buy!!!” tweet, must be feeling a little better off.

We acknowledge that we don’t have President Trump’s influence, as well as his global reach but, those of you who have followed our words, in a similar fashion as how investors recently flocked into the equity markets because of Trump’s recent “This is a great time to buy!!!” tweet, must be feeling a little better off.

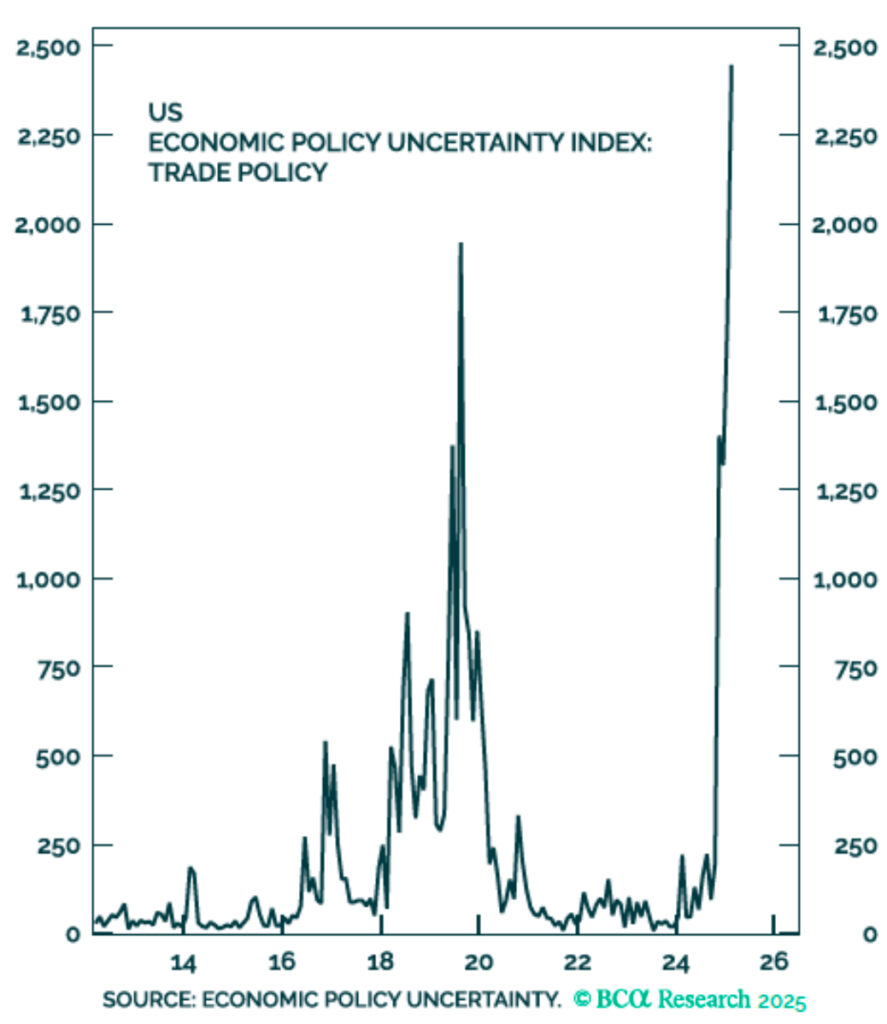

Up until now, and for a good cause, we have tried to downplay what has happened lately. However, the situation is very serious. The administration’s economic agenda can be summarized with a “3/3/3”: increasing domestic oil production by 3 million barrels per day, reducing the budget deficit to 3% of GDP, and achieving an annual GDP growth rate of 3%. Tariffs should, theoretically, serve the triple purpose of a) raising the Federal Government revenues (tariffs are a form of taxes) and thus lowering the deficit, b) allowing the administration to cut taxes on individuals and corporations, supporting GDP growth, and c) to stimulate domestic demand by bringing back home some supply chains that have been stolen by low-cost countries, such as China. Trying to steer the economy by managing interest rates, as the central bank must do, is already extremely complex. Now imagine the difficulty of having to reorganize it by acting on multiple factors at once! The program is inherently full of pitfalls and uncertainties. If, on top of that, it is implemented through unorthodox methods, it adds even more uncertainty to an economy that was already slowing down and is now facing drastic changes. No wonder investors have panicked.

The temporary pause on the tariffs (I hope this will still be true once you get to read this, early next week…) will allow countries to sit down and negotiate on possible concessions to make to the current administration. Yet, it is important to remember that a) 25% on cars and 10% reciprocal tariffs are still in place, and b) China is currently subject to a whopping 145% tariff (again, hoping this number doesn’t change soon) on any product it exports to the United States (U.S.). China is its third biggest commercial partner (after Mexico and Canada). In 2024, the U.S. imported almost 440bn USD worth of goods, and the total volume of trade between the two superpowers reached almost 600bn USD. Given China is imposing a 125% tariff on anything coming from the U.S., the commercial relationship between Washington and Beijing is pretty dire at the moment. This cannot be good for the world economy, including the U.S.

We have recently mentioned that the “spectre of a U.S. recession is no longer hiding quietly in the closet”. While the pause in the tariffs has closed the bedroom door, ensuring the spectre doesn’t reach the rest of the house, it does not send him back into the closet. This is because, as we have mentioned earlier, the U.S. economy was decelerating, and tariffs do nothing but accelerate the slowdown. The main areas of weakness remain unchanged: the manufacturing sector—once a key focus of President Trump’s economic agenda—has returned to sluggish growth after a brief period of improvement. The housing market is still unaffordable, and prices are not showing any signs of collapsing. To give you an interesting statistic: the percentage of outstanding mortgages with an interest rate above 6% has risen from 4% to almost 20% in just two years. This will eventually have an impact on the overall housing market, as the demand will be curbed unless interest rates begin to fall. Finally, the sentiment of the U.S. consumer is weakening. As a reminder, consumption makes up a large portion of the American GDP therefore, the expectations of U.S. households are very important in defining the future path of the economy. The weakness is likely the result of the uncertainty that emerged during the tariff-saga, and it follows a period during which excess savings have been depleted. Inflation expectations have begun to rise slightly again, but with wages taking the opposite direction as the labor market continues to cool down and the government support is fading under DOGE’s program.

We have recently mentioned that the “spectre of a U.S. recession is no longer hiding quietly in the closet”. While the pause in the tariffs has closed the bedroom door, ensuring the spectre doesn’t reach the rest of the house, it does not send him back into the closet. This is because, as we have mentioned earlier, the U.S. economy was decelerating, and tariffs do nothing but accelerate the slowdown. The main areas of weakness remain unchanged: the manufacturing sector—once a key focus of President Trump’s economic agenda—has returned to sluggish growth after a brief period of improvement. The housing market is still unaffordable, and prices are not showing any signs of collapsing. To give you an interesting statistic: the percentage of outstanding mortgages with an interest rate above 6% has risen from 4% to almost 20% in just two years. This will eventually have an impact on the overall housing market, as the demand will be curbed unless interest rates begin to fall. Finally, the sentiment of the U.S. consumer is weakening. As a reminder, consumption makes up a large portion of the American GDP therefore, the expectations of U.S. households are very important in defining the future path of the economy. The weakness is likely the result of the uncertainty that emerged during the tariff-saga, and it follows a period during which excess savings have been depleted. Inflation expectations have begun to rise slightly again, but with wages taking the opposite direction as the labor market continues to cool down and the government support is fading under DOGE’s program.

Much has been written about whether tariffs are inflationary or deflationary. We tend to believe the former are inflationary, at least in the beginning, and if not accompanied by fiscal austerity. However, shelter inflation is currently falling, and oil prices are tumbling; these two factors together should ensure that inflation expectations remain anchored, even if tariffs were to remain at their current levels. Anchored inflation expectations are very important because they allow the Federal Reserve (FED) to implement the necessary interest rate cuts in case the U.S. economy is clearly headed for a recession. Currently, the market is expecting roughly four cuts for 2025, with the first one in June, followed by another in July. This also signals that the recession probabilities have risen. Much will also depend on how companies react to the tariffs; the earnings season is just starting, and the next few weeks will shed more clarity on whether the companies’ management teams will pull the oars into the boat, or whether a positive attitude prevails.

Given Europe and China are the major targets of Trump’s tariffs, it is very difficult to assess how the two economies will adapt to the new duties. The starting point is similar, but the path that brought the two economies to their current state is completely opposite. Europe survives because of the encouraging performance of peripheral countries. Inflation is receding while wages continue to tick up, modestly supporting consumption. The central bank is ready to cut rates again but has signaled that any future cut will be data-dependent, especially after the U-turn of the German government with respect to fiscal spending. The risk is that the economy picks up again, setting an example for other nations that, however, are less virtuous in terms of their public finances. This, along with tariff negotiations are factors that the central bank will monitor closely when deciding the proper degree of monetary easing.

China, on the other hand, is still in a balance sheet recession but, the improvements noticeable towards the end of 2024 have been confirmed during the first quarter of this year. Some of the improvements came from a global front-running on tariffs, thus they will be reversed soon. Chinese banks are urged to lend but, with inflation close to zero, the real lending rate remains elevated, dragging down investments and consumption. The massive tariffs the U.S. has applied on Chinese goods will certainly make the recovery an arduous target to achieve; central bank’s monetary easing, a weaker currency, and perhaps fiscal easing by the central government are all tools needed to ensure the economy remains afloat. Nobody would benefit from a Chinese recession. Not even President Trump.

FIXED INCOME: TRUST IN THE U.S. SHAKEN (TEMPORARILY)

Everything that is happening at the geopolitical level is having meaningful consequences for financial markets. What has occurred recently is somewhat unique when compared to the post-Great Financial Crisis period. USD government bonds have initially skyrocketed, as investors craved safe-haven investments. The correlation between interest rates and equity returns remained negative, as should be during an economic crisis. However, it did not last long. During the second day of the equity market selloff, yields bottomed out at 3.86% and then soared a few days later to 4.50%. It is important to remember that the equity market is still under stress and that inflation expectations are well-anchored. So, what is happening? Difficult to say. There are many theories circulating, including plots and conspiracies. The truth we believe is very simple; there is a lot of uncertainty around, and the USD together with U.S. Treasuries appear to be less safe than they were before. At least, this is what prices are telling us.

For this reason, it is also difficult to speak about asset allocation and duration allocation. Once trust begins to erode, everything else starts to matter less. However, we believe this is just short-term turbulence and sooner rather than later, U.S. Treasuries will offer the protection they have offered in the past. For this reason, giving stagflation a very limited probability of happening, we find this to be a very attractive opportunity to increase government exposure and lock-in attractive yields. In this highly uncertain environment, our preferred credit exposure remains investment grade issuers, as fundamentals remain solid, and spreads have loosened towards historical averages.

Within the riskier buckets, high yield spreads have also started to widen. However, while equities are pricing in a 50% chance of a recession maturing during the year, high yield prices have not corrected as much, leaving valuations above historical averages. For this reason, we believe there will be more attractive entry points in the coming months. A similar rationale applies to emerging markets hard-currency bonds, especially in a world ruled by tariffs (emerging market countries are huge exporters to the U.S.). If investors would like to ramp risk up, we favor subordinated bonds and corporate hybrids, especially those of investment grade issuers, offering solid balance sheets, attractive yields, and fair valuations.

EQUITY: RELATIVELY MORE ATTRACTIVE, NOT YET A BARGAIN

The VIX Index (the volatility implied by the options traded on the S&P 500) has recently crossed the 60-mark; to put things into perspective, it reached 85 during the Covid equity meltdown, and 90 during the Great Financial Crisis. This is one of the most volatile moments of the past 50 years.

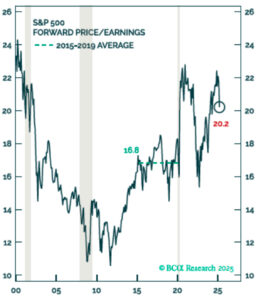

We have entered this correction – the S&P 500 is close to, but did not yet enter bear market territory – with equities showcasing one of the best profiles ever; peak margins, peak earnings growth, close-to-peak valuations. The correction has helped bring valuations lower. The 12-months forward price/earnings ratio (P/E) is trading at 20x, down from 22.5x a month ago. However, earnings have not yet been adjusted downwards substantially. We suspect that, as the earnings season kicks off, negative forward guidance will be the predominant theme during earnings calls, prompting analysts to quickly adjust their projections; margins and earnings expectations will therefore follow valuations lower.

Perhaps, from a trading perspective, this could be a good time to buy the dip – history shows that on average after a 15% correction, a rebound is in the cards. However, from a fundamental perspective, the chances of a recession are now higher than ever before, making an investment in equities very risky, at this stage. An underweight stance is therefore warranted, and more information is needed before ramping up risks in the portfolios again.

International equities, Europe in particular, could be the main beneficiary of the currently hasty environment. Valuations are nowhere near where they stand in the U.S., interest rates are not under attack, and Germany’s fiscal spending program could boost investments and (perhaps) lift productivity. As things stand, there are now more reasons to believe that the gap which has developed between the two regions over the past twenty years could start to reverse—supporting the case for making portfolios less U.S.-centric than before.

Currencies and Commodities: SAFE-HAVEN ASSETS STEALING THE SPOTLIGHT

Geopolitical decisions, a stronger dollar, and economic issues in China are all reasons that should manifest in a weak commodity market, but stubborn inflation will pressure the opposite way. Industrial metals may face some headwinds as the global economy slows down and tariffs exacerbate the situation, with metals linked to the electric vehicle market pressured as the latter suffers from overcapacity and falling demand.

Gold prices have remained resilient despite outflows from ETFs; this is most likely the result of long-term investors purchasing physical gold (central banks and institutional investors) despite rising real interest rates. The latest slump in the USD has further supported the yellow metal, which seems unstoppable. Despite its incredible run, we think gold will remain in the spotlight, with the USD debasement and U.S. Treasury selloff acting as a boost to demand. Conversely, oil is facing the perfect storm; rising output and the prospect of a U.S. recession have sent prices tumbling. If the latter continue to fall, US shale producers will become unprofitable, curbing US shale oil output and thus putting a floor to how low prices can fall.

The recent pullback in interest rate differentials, and the turmoil we have discussed at length, has weakened the USD (DXY Index). A short-term rebound is highly likely. On the contrary, the recent spending announcement of the German government has led to an increase in EUR yields, as expectations for both higher growth and higher bond supply were being priced in. Consequently, the EUR has appreciated against major currencies, including the USD.

Longer-term, and based on the real effective exchange rate, we continue to see the USD as overvalued, with the CHF and EUR as slightly undervalued.

Document sources: Capital Economics, BCA, 3Fourteen Research, Creditsight, Empirical, Vontobel, Factset, Refinitiv IBES, Hussman Strategic Advisors, Yardeni, Bloomberg.

Document sources: Capital Economics, BCA, 3Fourteen Research, Creditsight, Empirical, Vontobel, Factset, Refinitiv IBES, Hussman Strategic Advisors, Yardeni, Bloomberg.

CONTACT US:

Edoardo Mango, CIO

LFA – Lugano Financial Advisors SA

Via F. Pelli 3

6900 Lugano, Switzerland

+41 91 922 69 16

www.lfa.ch

DISCLAIMER:

The information contained in this presentation is the opinion of LFA and does not reflect the view of any other person or entity. Further information with regards to LFA – Lugano Financial Advisors SA is provided on the ADV Part 1 and Part 2 (Brochure and Supplement).

The information provided is believed to be from reliable, accurate and complete sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation.

Past performance is no guarantee of future performance. LFA is an investment adviser registered with the U.S. Securities and Exchange Commission and only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

Copyright

Unless otherwise provided, all the content of this document is covered by Copyright. All the rights pertain to LFA. The material set forth herein has been prepared in a private and confidential perspective, with the sole purpose of consultation. Every reproduction of the material, even if only partially, in any form, written and/or electronic, is solely allowed upon prior explicit consent granted by LFA.